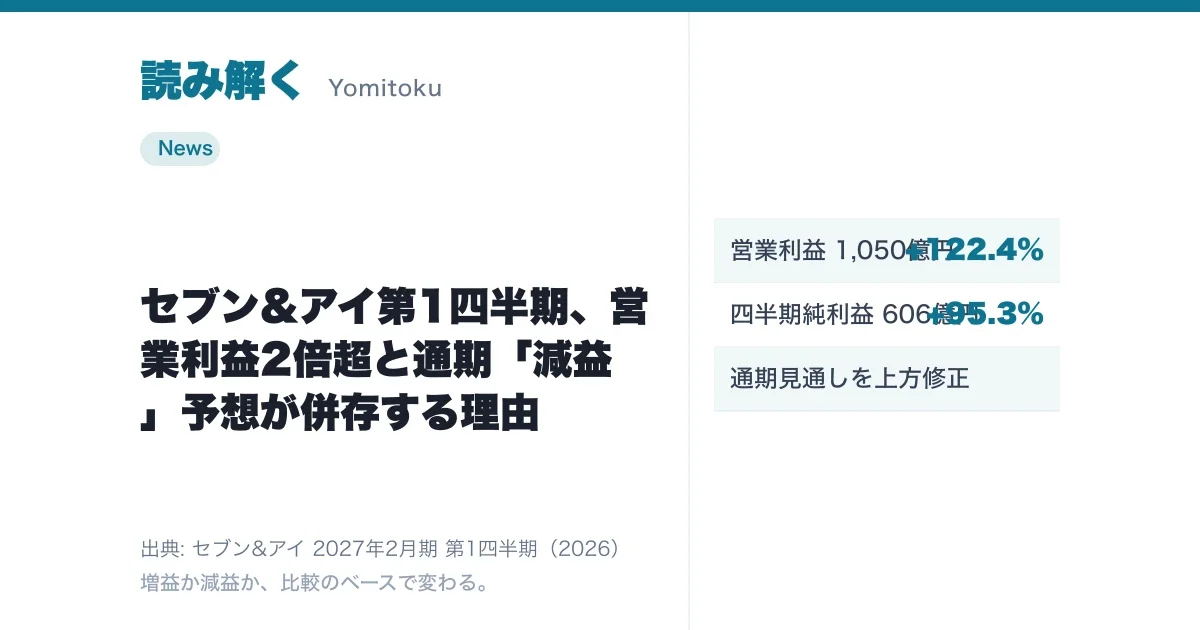

Seven & i Holdings released its first-quarter earnings summary for the fiscal year ending February 2027 (which the company calls “FY2026”) on July 9, 20261. Operating profit rose 122.4% year on year to ¥105.0 billion, and net profit attributable to owners of the parent climbed 95.3% to ¥60.6 billion. President and CEO Stephen Dacus commented that consolidated operating profit and EPS “more than doubled year on year and reached a record high”1.

Yet some reports described the same set of results as a “decline in net profit.” How can a single earnings release produce headlines as opposite as “record-high growth” and “a decline”? The answer lies in the corporate restructuring the company is carrying out, and in which “basis of comparison” the figures use. This article reads the difference straight from the primary disclosure.

Q1 operating profit of ¥105.0bn, driven by North American fuel

Start with the actual Q1 results. Much of the ¥105.0 billion in operating profit came from the North American convenience-store business. U.S. subsidiary 7-Eleven, Inc. (SEI) saw existing-store merchandise sales rise 1.4% year on year and total chain sales grow 1.2% to about ¥2.38 trillion, with operating profit of ¥88.0 billion1. The company attributes this gain to “an improvement in fuel gross profit against the backdrop of significant volatility in the petroleum-product market through the quarter, as across the industry”1. North American convenience stores sell gasoline at the storefront, so swings in petroleum-product prices lifted profit.

In Japan, Seven-Eleven Japan (SEJ) posted existing-store sales up 2.0% year on year on higher spend per customer and improved traffic, a merchandise gross margin up 0.3 point to 32.0%, and total chain sales up 2.4% to about ¥1.37 trillion1. Domestically the business held firm while continuing to invest in fresh food and store renovation.

What is the “122.4% increase” being compared against?

The key point is what that opening “122.4% increase” is measured against. In the footnote to its highlights, the company states that “the year-on-year comparison excludes the effect of the deconsolidation of York Holdings and Seven Bank”1. The company is restructuring to remove York Holdings — which runs its superstore business — and Seven Bank from its scope of consolidation. Comparing directly against prior-year figures that still included them would mix the effect of swapping businesses in and out with the actual change in performance. So the company discloses two versions: a “real basis” that strips out the restructuring effect, and an “accounting basis” that lines up the reported figures as they are.

| Item | Q1 actual (¥100M) | YoY (real) (%) | YoY (accounting) (%) |

|---|---|---|---|

| Operating revenue | 23,788 | 102.4 | 85.7 |

| Operating profit | 1,050 | 222.4 | 161.4 |

| Net profit attributable to owners | 606 | 195.3 | 123.6 |

As the table shows, operating revenue is flat at 102.4% on a real basis but looks like a “decline” at 85.7% on an accounting basis1 — because York Holdings’ and Seven Bank’s revenue is in the prior-year figure but not the current one3. Operating profit, by contrast, grew sharply on both bases: 222.4% (about 2.2x) on a real basis and still 161.4% (about 1.6x) on an accounting basis. For Q1, in other words, it was an increase in profit regardless of which basis you use.

The upward guidance revision and the “decline” headline

Based on the Q1 results, the company raised its full-year guidance for the year ending February 2027, lifting the consolidated operating-profit outlook by ¥20.0 billion and the consolidated net-profit outlook by ¥8.0 billion versus the initial plan1. The revised full-year guidance is as follows.

| Item | Revised (¥100M) | Revision (¥100M) | YoY (real) (%) |

|---|---|---|---|

| Operating revenue | 104,300 | 9,820 | 109.7 |

| Operating profit | 4,250 | 200 | 110.5 |

| Net profit attributable to owners | 2,780 | 80 | 109.1 |

| EPS (¥) | 120.89 | 3.47 | 116.9 |

Full-year net profit attributable to owners of the parent is guided to ¥278.0 billion after the revision, up 9.1% (109.1%) year on year on a real basis1. But line that same ¥278.0 billion up against the pre-restructuring prior year on an accounting basis, and it becomes 95.0% — roughly a 5% decline1. That accounting-basis figure is what some outlets meant by “a decline.” Once the sizeable superstore and banking businesses leave the scope of consolidation, their profit also drops out of the prior-year comparison, so the very same ¥278.0 billion can be described as either an increase or a decrease.

When reading earnings, you have to check which basis a “year-on-year” figure is calculated on — not just the headline number, but down to the footnotes. For a company reshuffling its business portfolio, the very ground of comparison shifts, so even the sign of the growth rate can change with how it is presented. Seven & i’s disclosure this quarter is a textbook example.

How to read the “quality” of the profit gain

One more thing worth noting is the nature of the Q1 profit driver. The improvement in fuel gross profit that lifted SEI’s ¥88.0 billion operating profit stems from volatility in the petroleum-product market1. Market factors can be a tailwind or a headwind, so this will not necessarily continue. Indeed, the company itself says that for the full-year outlook it “assumes that fuel-market conditions will normalize somewhat in the second half”1. Q1’s strong growth carries a one-off market element on top of structural initiatives such as store renovation and fresh-food investment (the “North Star” plan in North America) — a distinction worth drawing before taking the numbers at face value.

Through the restructuring the company is concentrating on its convenience-store business, and CFO Tetsuya Takagi commented that it will “continue disciplined capital allocation” and improve ROIC1. While businesses are being swapped in and out, growth rates are prone to diverging from the underlying reality. When both a “real” and an “accounting” basis are disclosed, as in this quarter, reading the two side by side is the practical way to avoid misreading the results.

Sources

- FY2026 Q1 Earnings Summary (PDF) - Seven & i Holdings official (July 9, 2026)

- FY ending Feb 2027 Q1 Earnings Summary news release - Seven & i Holdings official (July 9, 2026)

- Seven & i earnings / Mar–May operating profit +61.4%, full-year raised on overseas convenience-store gasoline gains - Ryutsu News (July 9, 2026)