Fast Retailing released its third-quarter earnings report for the year ending August 2026 on July 9, 20261. For the first nine months (September 2025 to May 2026), revenue rose 17.1% year on year to ¥3.065 trillion and operating profit rose 36.2% to ¥614.3 billion, which the company described as “a record high for the consolidated group as a whole”1. It also revised its full-year guidance upward.

“Higher revenue and profit, a record, an upward revision” reads as unambiguously strong — but two things are worth reading closely: which businesses and regions actually earned that profit, and the difference between the two profit measures that appear in the company’s accounts, “business profit” and “operating profit.” This article breaks down the internals from the figures in the earnings report.

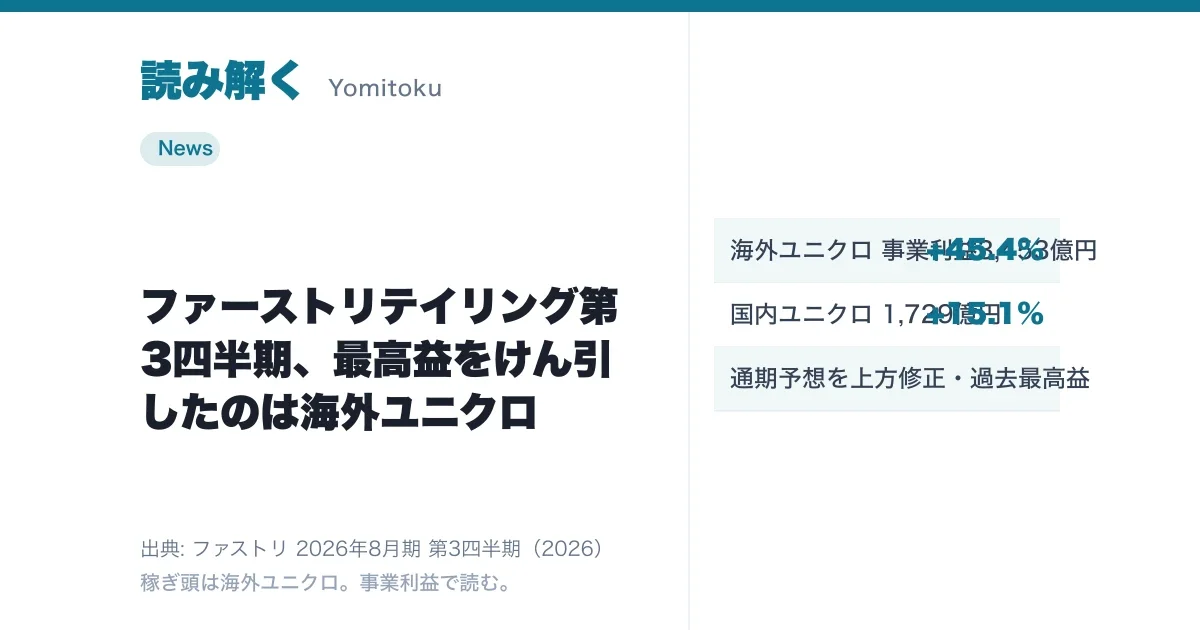

The engine is overseas UNIQLO — roughly double Japan’s business profit

The company reports across four segments: UNIQLO Japan, UNIQLO International, GU, and Global Brands. Line up nine-month revenue and business profit by segment, and it becomes clear where the profit pillar sits1.

| Segment | Revenue (¥100M) | Business profit (¥100M) | Business profit YoY (%) | Margin (%) |

|---|---|---|---|---|

| UNIQLO International | 18,340 | 3,453 | 45.4 | 18.8 |

| UNIQLO Japan | 8,676 | 1,729 | 15.1 | 19.9 |

| GU | 2,656 | 321 | 28 | 12.1 |

| Global Brands | 963 | 19 | -33.4 | 2 |

UNIQLO International earned business profit of ¥345.3 billion, up 45.4% year on year — roughly double UNIQLO Japan (¥172.9 billion, up 15.1%)1. The company says Mainland China grew revenue with double-digit profit growth, and both North America and Europe posted double-digit gains in revenue and profit, citing store expansion including a flagship in Chicago as it built brand strength1. UNIQLO Japan also held firm, with existing-store sales up 9.9%1 — but by both scale and growth rate, Fast Retailing’s profit growth is now led by the overseas business.

The one segment with declines in both revenue and profit was Global Brands (Theory, Comptoir des Cotonniers, and others), with revenue of ¥96.3 billion (down 4.2%) and business profit of ¥1.9 billion (down 33.4%)1. The company disclosed that in the Comptoir des Cotonniers / Princesse tam.tam business it is consolidating unprofitable stores, with the store count at the end of May roughly halving from 144 a year earlier to 771. Even when the whole company is doing well, results differ by business.

How “business profit” differs from “operating profit”

A common stumbling block in reading this company’s results is the pair of similarly named measures, “business profit” and “operating profit.” The earnings report defines business profit as “revenue − cost of sales − selling, general and administrative expenses”1 — the profit from the core activity alone of buying goods, selling them, and running stores and headquarters. Nine-month business profit was ¥592.7 billion, up 33.6% year on year1.

Operating profit, by contrast, was ¥614.3 billion (up 36.2%), ¥21.6 billion larger than business profit1. The gap arises because operating profit adds items that business profit excludes. The income statement in the earnings report shows what they are: “other income” of ¥24.3 billion (including foreign-exchange gains arising from operating transactions), less “other expenses” of ¥3.7 billion (losses on retirement of fixed assets, impairment losses, and the like), plus ¥1.1 billion in profit from equity-method investments1. Operating profit, in other words, also captures one-off gains and losses that arise around the core business.

So where does the interest earned on the company’s cash pile go? The company says net finance income was a positive ¥43.8 billion — net interest of ¥37.8 billion plus ¥5.9 billion in foreign-exchange gains from the translation of foreign-currency assets and other items1 — but this enters not operating profit but the next stage down, profit before income taxes (¥658.2 billion)1. If you want to gauge the strength of the business itself, look at business profit; for earnings including one-off items, operating profit; and to capture finance and FX effects as well, pre-tax profit. Each stage measures something different, so when comparing against prior years or peers, you need to line up like with like.

The upward revision — check the reason too

The company also raised its full-year (year ending August 2026) guidance. Before and after the revision:

| Item | Previous (¥100M) | Revised (¥100M) | Change (%) |

|---|---|---|---|

| Revenue | 39,000 | 39,700 | 1.8 |

| Business profit | 6,900 | 7,100 | 2.9 |

| Operating profit | 7,000 | 7,300 | 4.3 |

| Pre-tax profit | 7,400 | 7,800 | 5.4 |

| Net profit attributable to owners | 4,800 | 5,000 | 4.2 |

The full-year forecast for net profit attributable to owners of the parent was raised 4.2%, from ¥480.0 billion to ¥500.0 billion1. Worth checking is the reason for the revision. The company cites “(1) reflecting corporate performance through June, and (2) revising the exchange rates used to calculate fourth-quarter business estimates to bring them in line with current actual rates”1. In other words, the upgrade reflects not only an upside in actual results but also a revision to the assumed FX rates applied in the fourth quarter. That operating profit and pre-tax profit were revised up by relatively larger margins may reflect non-core factors such as FX gains. Reading not just the headline size of a revision but whether its internals are core growth or a change in assumptions makes the underlying reality easier to grasp.

The company also guides an annual dividend of ¥640 per share for the year ending August 2026 (¥320 interim and ¥320 year-end), an increase from ¥500 the prior year1. Break down the record results and the upward revision by business, region, and profit measure, and a picture emerges: growth centered on overseas UNIQLO, and profit whose appearance is also swayed by finance and FX.

Sources

- Q3 FY ending Aug 2026 Earnings Report (IFRS), consolidated (PDF) - Fast Retailing official (July 9, 2026)

- Fast Retailing earnings / Sep–May operating profit +36.2%, brand strength up on overseas flagships - Ryutsu News (July 9, 2026)

- Fast Retailing raises full-year net-profit forecast by 4%, lifts record outlook - Kabutan News (July 9, 2026)